Chargement...

Chargement...

A real notarial invoice from Songon Audoin (500 m² at 15,000 FCFA/m²): 1,462,275 FCFA in fees for 7,500,000 FCFA of land, or 19.5%. A line-by-line breakdown, with every amount cross-checked against official regulations, and what this levy reveals about the development of unserviced areas.

Need a land expert?

Speak with an advisor for free. Response within 2 hours.

A real notarial invoice, reconstructed line by line from official texts. Here's what a land sale deed truly costs in Côte d'Ivoire, and what it reveals about the development of our emerging areas.

We budget for the price of the land, rarely for the cost of the deed. A real notarial invoice from April 2026, broken down here line by line, shows that in Côte d'Ivoire acquisition fees can represent up to 20% of the price of a land asset on modest transactions: 1,462,275 FCFA in fees for a plot of 7,500,000 FCFA (500 m² at 15,000 FCFA/m² in Songon Audoin), i.e. 19.5%. Every line of this invoice corresponds to an official text, and we cite them all. Contrary to what the expression "notary fees" suggests, more than half of the amount goes into public coffers. This level of taxation, applied to areas that are neither serviced nor habitable as they stand, hampers formalisation where it is most useful: it is only sustainably justified if the expected public investments (roads, water, electricity, sanitation) actually arrive in the area; otherwise, the burden of development weighs twice on private investors. In the meantime, Capital Foncier's response comes down to two principles: a flat 20% provision built into the budgets of its projects, and the full refund of any surplus to the investor when the final invoice is lower.

April 2026, an Abidjan notary's office draws up the invoice for the sale of an urban plot. The figures, with parties anonymised:

| Item | Amount |

|---|---|

| Sale price (500 m² × 15,000 FCFA/m²) | 7,500,000 FCFA (≈ €11,400) |

| I. Duties owed to the State | 781,025 FCFA |

| II. Disbursements | 170,000 FCFA |

| III. Notary's emoluments and fees | 511,250 FCFA |

| Total provision requested | 1,462,275 FCFA (≈ €2,230) |

| Total acquisition cost | 8,962,275 FCFA (≈ €13,700) |

| Fees / sale price | 19.5% |

The price per square metre is nothing exotic: 15,000 FCFA/m² is the reference value published by the Directorate General of Taxes (DGI) for the Audoin neighbourhood of Songon in the 2023 edition of its scale of market values for urban land (Dabou regional directorate booklet, under which the municipality of Songon falls). These scales are indicative minimum values, revised every three years; a 2024-2026 edition was published in September 2024. This sale was therefore made at the tax reference floor for the area. And yet the fees still approached a fifth of the price.

Capital Foncier Diagnostic. Before you commit to a plot, an advisor checks the proposed price against the DGI scale for the area and calculates the total acquisition cost, deed fees included. Get my diagnostic — response within 2 hours.

What makes this invoice valuable is that it can be reconstructed down to the franc from official scales. Demonstration:

| Invoice line | Amount (FCFA) | Applicable text | Verification |

|---|---|---|---|

| Registration | 555,000 | Transfer duty of 4% (art. 760 CGI) + capital gains levy on the seller of 3.4% (art. 762 CGI: 17% of a flat-rate capital gain of 20% of the price) | 300,000 + 255,000 = 555,000 |

| "Land tax" | 90,000 | Land publicity tax of 1.2% collected at the transfer formality | 7,500,000 × 1.2% = 90,000 |

| Proportional emoluments | 225,000 | Notaries' tariff, decree no. 2013-279 of 24 April 2013: 3% on the price band up to 10 million | 7,500,000 × 3% = 225,000 |

| VAT (18%) | 92,025 | Art. 359 CGI: standard-rate VAT on the notary's emoluments (not on the land) | 511,250 × 18% = 92,025 |

| Certificate of ownership | 15,000 | Transfer formality fees (DGI fee schedule) | 15,000 |

| Fixed duties, land status reports, stamps | 29,000 | Fixed duty 3,000, land status report 3,000 (× 2), stamps | in line with published tariffs |

Three observations. First, the "Registration" line aggregates two distinct taxes: the 4% transfer duty owed by the buyer, and the 3.4% capital gains levy which the law places exclusively on the seller but which passes through the office's accounts at the time of the formality. Second, the "Land tax" line on this invoice is not the annual property tax: its amount corresponds exactly to the 1.2% land publicity tax linked to the transfer. Finally, the 18% VAT never applies to the land itself in a sale between private individuals: it is levied on the notary's emoluments, to the franc on this invoice.

The rest relates to the specific work on the file: disbursements (170,000 FCFA), special fees (101,250 FCFA), the notary's emolument for the application for the land ownership transfer certificate (CMPF, 75,000 FCFA, not to be confused with the official cost of the CMPF itself, of around 15,000 FCFA, recorded on the "certificate of ownership" line), registers and formalities (100,000 FCFA) and land requisitions (10,000 FCFA).

On this invoice:

The exact term would be "acquisition fees". The notary, for their part, provides what has no substitute: the authentic deed, the only valid method of transferring Ivorian urban land since Ordinance 2013-481. A "private agreement" between individuals does not transfer ownership of an urban plot and is not enforceable against you. These fees are not an arbitrary toll; they are the price of your ownership being enforceable. The question lies elsewhere: their relative weight, and what it funds.

Let's break down the 1,462,275 FCFA according to their mechanics:

That is the whole explanation for the "up to 20%": the fixed base weighs all the more heavily as the price is low. On a 30 million FCFA plot, the same fee structure would produce a ratio of around 13%, since the notary's emoluments are themselves degressive by band (3% up to 10 million, then 2%, 1% and 0.5% above 90 million). The smaller your land budget, the greater the relative share of the fees. A diaspora investor budgeting €11,400 for their 500 m² plot must actually plan for close to €13,700 to come out as owner, deed in hand.

We must be precise: 19.5% is not the national average. In its latest Doing Business (2020, the last edition before the report was discontinued), the World Bank measured an official property transfer cost of 7.1% of the asset value in Côte d'Ivoire, on a standardised transaction of around 60 million FCFA, excluding VAT and the capital gains levy. The sub-Saharan Africa average was 7.3%, OECD 4.2%, Senegal 7.1%, Benin 3.4%, Burkina Faso 11.9%.

Two points of perspective:

This must be said calmly, because it is a real land policy issue: this level of transaction costs raises questions when it applies to areas that are neither serviced nor habitable as they stand.

In Songon Audoin, as in many extension areas of Greater Abidjan, the buyer of a plot at 15,000 FCFA/m² is purchasing potential: across much of these localities, there are no paved local roads, no water supply, no electricity connection. The use value will come with servicing. Yet the fee mechanism applies, as we have seen, proportionally more harshly than for a plot fitted out in an established area.

Economic research is clear on this mechanism. In Rwanda, a study published in Land Use Policy (2021) identifies registration cost as the main reason for a return to informality: when fees exceed owners' willingness to pay, transactions stop being registered and the registry degrades. In Dar es Salaam, a World Bank experiment (2014) shows that demand for formal titles is highly price-sensitive: when it falls, formalisation takes off. And the Ivorian starting point is low: about 1% of the country's rural land has a land document (World Bank, 2024), and the Definitive Concession Decree (ACD) system had only produced 34,460 cumulative decrees as of end-2023 for the whole country, including around 8,900 for Abidjan, an agglomeration of several million inhabitants.

The consequence is a public policy paradox: the proportionally heaviest levy strikes the areas and amounts where formalisation is most fragile. Three effects follow:

Let's be balanced: this tax is not illegitimate in itself. Ivorian law even explicitly organises the link between land tax and public services. The tax on land assets is largely returned to local authorities; the Ministry of Finance describes it as the bulk of the tax administration's support to municipalities. The road, hygiene and sanitation tax was "established with the aim of providing the body responsible for household waste management with the resources necessary to carry out its mission" (explanatory memorandum, 2026 tax annex). And the law requires municipalities to allocate a fraction of their revenue to an investment fund, a fraction that the 2026 tax annex has just raised.

The implicit contract is therefore clear: today's levy funds tomorrow's infrastructure. When it is honoured, the cycle is virtuous: the buyer pays, the area is equipped, use value arrives, the tax base expands, and everyone gains.

Around Songon, part of this contract is visibly being executed, and this must be documented honestly. Three national road corridors funded over the recent period directly affect the municipality: the Western motorway exit (Gesco–Jacqueville junction, 19 km crossing Songon, 66.3 billion FCFA, opened in January 2024), the section of the Y4 ring motorway ending at the Jacqueville junction (project of around 217 billion FCFA in total, almost complete in early 2026), and the Songon–Dabou–Grand-Lahou section of the coastal road (part of a 308 billion FCFA programme). Individual facilities are also arriving, such as the water tower inaugurated at Songon Gravier Adiapo-Moronou in November 2025.

But the fine link in the contract, the internal servicing of neighbourhoods, which makes a plot habitable, remains the blind spot. Our research has identified no costed State programme for servicing Songon's neighbourhoods over 2021–2026: the government's social electrification programme has focused on the north of the country, the major Greater Abidjan sanitation project targets Yopougon, Abobo and Grand-Bassam, and the water plant located in the territory of Songon itself (Adonkoi) supplies Abobo, Anyama and Yopougon. The State itself acknowledges the tension: the explanatory memorandum of the 2026 tax annex admits that "the applicable rates still appear high" in land matters, and consequently caps tax increases.

As long as this link is missing, the equation is uncomfortable: the private investor pays twice. Once at the deed, nearly 20% in fees on small amounts; a second time on the ground, by financing themselves the borehole, solar energy, access. It is the burden of development transferred onto the very people expected to formalise and build up the area.

The principle of modulated land taxation is nothing exotic in Ivorian law. The legislator already modulates:

Extending this logic to transfer duties in non-serviced areas, a reduced rate before the arrival of networks, the full rate once the area is equipped, would be a formalisation lever consistent with the trajectory embarked on since 2013, when the State divided the transfer duty by 2.5 precisely to stimulate formal transactions. This is a possibility Capital Foncier contributes to the debate, as an industry player. In the meantime, our response is the one that depends on us.

In the acquisition budgets presented on our projects, two principles apply:

This mechanism works even more in the investor's favour as the amount increases: since the real fee ratio decreases with transaction size (around 13% at 30 million versus 19.5% at 7.5 million), the gap between the flat provision and the real invoice, and therefore the refund, tends to grow with the ticket.

No. The official reference measurement (Doing Business 2020) gives 7.1% on a transaction of around 60 million FCFA. But this figure excludes VAT and the capital gains levy, and above all it is calculated on a large asset: flat-rate components weigh proportionally more on small prices. On the case documented here (7,500,000 FCFA), fees reach 19.5%; on a 30 million transaction, the order of magnitude falls back towards 13%. Hence the value of a pro forma invoice specific to your file.

Force of habit. On the invoice analysed, 53% of the total are public duties and taxes, 35% remunerate the notary's office (according to a tariff set by decree since 2013) and 12% cover the file's disbursements. "Acquisition fees" would be more accurate.

The notary requests a provision before the deed, calculated broadly to cover duties, disbursements and emoluments. After the formalities are completed, the office renders account: if the provision exceeds the actual fees, the surplus is refundable. In Capital Foncier projects, this refund to the investor is systematic and full, with supporting documents.

It is the reference value published by the DGI for the Audoin neighbourhood of the Songon municipality in the 2023 edition of its scale of market values for urban land (Dabou regional directorate booklet; Songon falls fiscally under DR Dabou, not the Abidjan directorates). A word of caution: these are indicative minimum values that serve as a tax floor, not market ceiling prices. The scale is revised every three years; a 2024-2026 edition was published in September 2024.

No, and it should not be considered. Article 673 of the CGI bases duties on the stated price or on the actual market value if higher, and the administration relies on the DGI scale as the minimum reference. Under-declaration is recalculated, increased where appropriate, and legally weakens your acquisition. The security of a deed also lies in its truthfulness.

Not on the price of the land in a sale between private individuals. The 18% VAT (art. 359 CGI) applies to the notary's emoluments and fees, not to registration duties or disbursements, which are excluded. On the invoice analysed: 18% × 511,250 FCFA of emoluments = 92,025 FCFA of VAT, to the franc.

Yes, but after acquisition and with recent relief: for a bare urban plot, the rate has fallen from 1.5% to 1% of the market value, and newly acquired plots benefit from a two-year exemption (2025 tax annex). On a 7.5 million plot in Songon Audoin, expect around 75,000 FCFA per year at the end of this period.

A Capital Foncier advisor calculates the total cost of your acquisition (price, deed fees, provision and refund terms) before any commitment.

Book an appointment — discovery consultation.

Documented case

Fiscal and tariff texts

Élargissez votre lecture avec d'autres facettes du foncier ivoirien.

Five bilateral tax treaties, one notable absence (USA-CI), four mandatory forms (2047, 2044, T1135, 8938): navigating the cross-border taxation of land investment in Ivory Coast from the diaspora. Educational guide, not personalized tax advice.

Lire l'article

L'ACD n'est pas un titre « en dessous » du Titre Foncier. Le TF est créé pendant la procédure ACD par la Conservation de la Propriété Foncière et des Hypothèques (CPFH). Démonstration juridique, 11 étapes officielles, 5 erreurs que les blogs concurrents continuent de diffuser.

Lire l'article

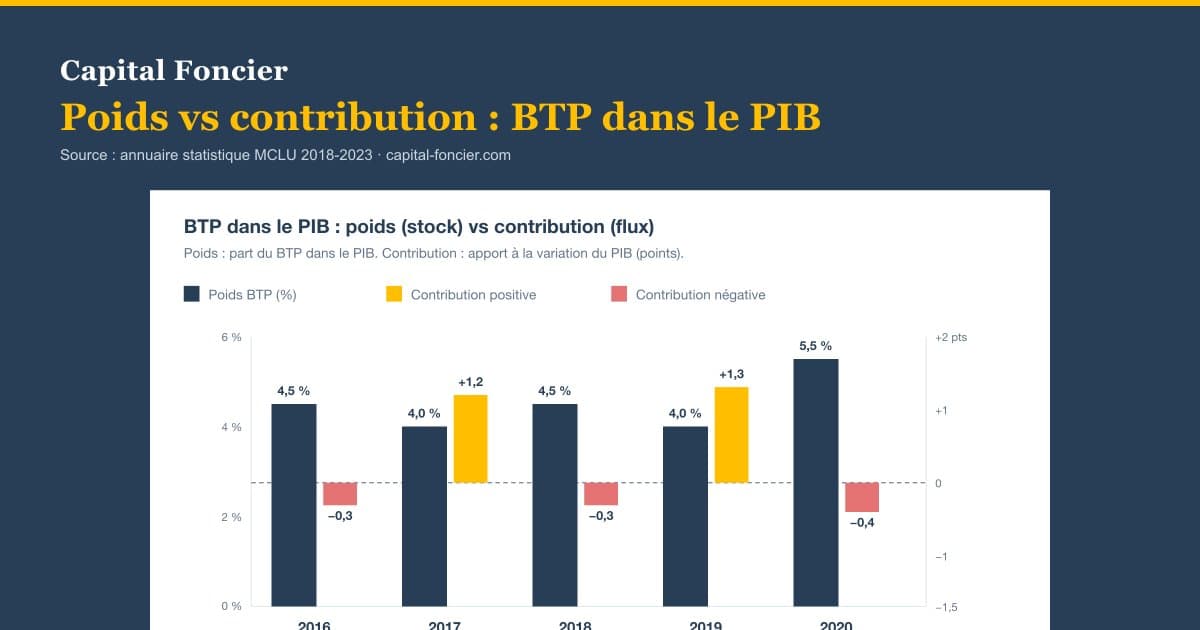

Le BTP ivoirien pèse 4 à 5,5 % du PIB. Il a contribué jusqu'à 1,3 point à la croissance en 2019. Ces deux chiffres disent des choses différentes et se lisent différemment. Décryptage pour investisseurs et acquéreurs qui veulent comprendre l'économie foncière.

Lire l'article